Understanding Great Bond Market Sell-Off

A Primer with Some Prospects

This report examines the background to the bond market. It explains the reasons why we have been bearish of duration (longer dated bond tenors) throughout this year, despite what has often been a backdrop of recovering Global Liquidity. We remain worried by the extremely depressed term premia component of bond yields.

We make the following key points: (1) the best way to decompose yields is into two moving-parts: policy rate expectations and term premia; (2) term premia explain the bulk of post-GFC movements in US Treasury yields; (3) the recent rise in US nominal yields has little to do with US economic strength, and (4) extremely depressed term premia are dangerous because they could easily add 100bp from here, threatening 6% 10-year Treasury yields and destroying precious collateral.

Digging Inside the Bond Yield

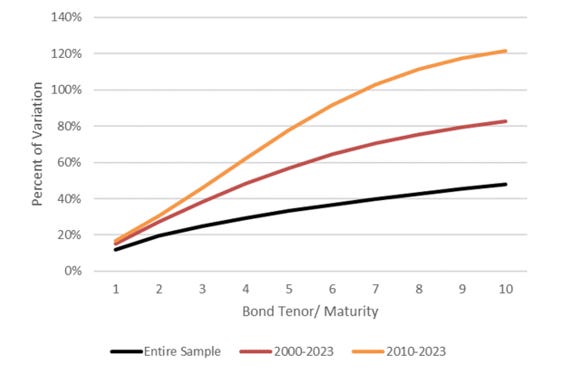

Nominal bond yields are most often split into two moving parts: (1) a real yield component, e.g. TIPS (Treasury Inflation Protected Securities), and (2) a break-even inflation component. Using history and experience, analysts project these components forward to assess prospective bond returns. However, we find this method inaccurate and misleading, Instead, we prefer to decompose bond yields into: (1) expected future policy rates over the term of the bond, and (2) a term premium component.

Chart 1: Contribution of Term Premia to Yield Variation By Tenor

Keep reading with a 7-day free trial

Subscribe to Capital Wars to keep reading this post and get 7 days of free access to the full post archives.