The Risks Ahead

An Outline of Four Major Faultlines

Recapping the Liquidity Approach

By emphasizing systemic refinancing dynamics over traditional valuation metrics, we have an unconventional perspective on financial markets. Our Global Liquidity framework underscores how today’s markets make up a huge collateralized debt-refinancing system, not a capital allocation mechanism. The 2025-28 ‘debt maturity wall’, combined with deteriorating credit quality and a worrying Fed policy lag, sets the stage for a potential future financial crisis. Looking through the current ‘Trade War’, the bigger ‘Capital War’ will be ultimately won by whoever controls the global collateral supply—and right now, that battle is looking less certain.

Our liquidity-based approach flips traditional economics and finance by focusing on debt refinancing mechanics rather than fundamentals and equilibrium. Instead of viewing markets as efficient capital allocators, we see them as fragile, collateral-driven systems where rollover risk, duration mismatches and safe asset shortages dictate stability—not interest rates or traditional valuation metrics. Central Banks need to act as collateral managers (‘dealers of the last resort’), pro-cyclical feedback loops dominate and crises emerge from liquidity crunches, not mis-pricing. Unlike traditional models, which assume self-correcting markets, our framework reveals a financial system that constantly skirts collapse, becomes reliant on policy intervention to sustain the debt-refinancing mechanism. The key metric isn’t GDP, interest rates or inflation—rather Global Liquidity: the interplay of asset supply, duration, and the hidden fragility of private credit chains.

We focus on how large investors and credit providers behave within system-wide constraints—such as liability durations, regulatory limits and collateral scarcity—rather than analyzing the merits of individual securities in isolation, which is traditional finance. We view financial markets primarily as a vast debt-refinancing mechanism rather than a new capital-raising system, where Global Liquidity (e.g. the ratio of financial asset supply to their duration) becomes the key metric, transcending the traditional focus on interest rates. This framework highlights how collateral shortages, pro-cyclical feedback loops, and the dominance of safe assets (like US Treasuries) shape global liquidity cycles, with refinancing demands driving a roughly 65-month periodicity that aligns with global debt maturity structures. The approach emphasizes flow of funds and explains phenomena like the dollar premium, volatility spikes during ‘Risk-Off’ episodes, and why monetary policy transmission often differs from textbook models.

Consider how in 2008, the liquidity-framework highlighted the collapse of shadow banking collateral chains (e.g., repo markets, MBS), whereas traditional economics blamed irrational exuberance and flawed risk models. Evidence how the US Fed’s 2019 repo market intervention wasn’t about too high interest rates but collateral scarcity (banks lacked Treasuries to meet regulatory demands). Traditional models missed this entirely. Consider also why the 2025 debt maturity wall isn’t a concern for traditional models (which assume availability of liquidity and smooth roll-overs), but our framework sees it as a potential liquidity sink that crowds out new lending. Further, take the Bank of England’s 2022 gilt crisis intervention. This wasn’t about too high rates but pension fund collateral calls—a liquidity dynamic traditional frameworks missed. Lastly, think about how the early-2020 dash for cash (when even gold sold off) showed dollar liquidity surpassing all else—a systemic insight traditional models ignored.

Traditional economics and finance struggle to explain:

Why inflation stayed low post-2008 (A: collateral glut suppressed velocity).

Why rate hikes do not always crash markets (A: private credit and shadow banking bypass traditional channels).

Why the dollar strengthens in crises (A: global system is a dollar-funded collateral pyramid).

Why an inverted yield curve may no longer signal recession (A: term premia effect)

Instead, our framework sees markets as complex and fragile, not as some textbook-based efficient pricing mechanism. This is why it can also explain recent events:

2019 repo crisis (collateral shortage).

2020 Treasury market freeze (dealer balance sheet constraints).

2022 UK gilt meltdown (liability-driven investing feedback loops).

Traditional economics and finance assume that markets trend toward equilibrium. Our approach shows they constantly skirt collapse, unless liquidity is forcefully injected by policy makers. This isn’t just a different model, it is a fundamentally different world-view, one that prioritizes financial plumbing and engineering over fake notions of fundamental value.

In short, traditional economics and finance asks: ‘What is the right price?’ Instead, our liquidity-based approach asks: ‘Who needs to buy and with what collateral?’ The difference is the gap between textbook theory and real-world crises….crises never occur in textbooks!

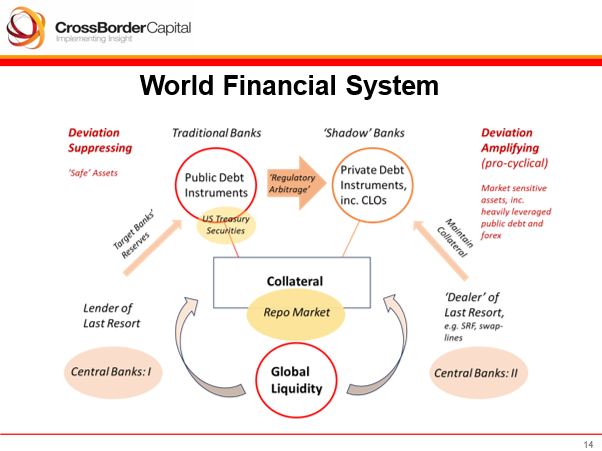

The majority of financial crises are triggered by the inability to refinance maturing debts. Financial intermediation seeks to speed up the turnover of capital through maturity transformation. However, maturity risk is simply transformed into credit risk, through overlapping balance sheets and lengthening collateral chains, or into forex risk via offshore lenders and currency swaps. So risk is never eliminated, but becomes ever more concentrated in credit markets. This forces periodic interventions by Central Banks to stabilize the system, either by injecting new liquidity (i.e. ‘lender of the last resort’), or increasingly by managing and improving collateral values (i.e. dealer of the last resort’).

Over time, and encouraged by collateral shortages and often heavy-handed regulation, the World financial system leans more heavily on to private sector collateral, often ignoring its greater associated credit risks. This both explains cycles and it worryingly highlights where markets stand now given the growing odds of outright economic recession. See diagram:

We have warned that even if Trump 2.0 ends up ‘winning’ a Trade War, America risks losing the bigger Capital War. Our concerns are four-fold:

(1) Rapidly slowing World business activity will sour corporate credits, raising default risks

(2) The US Federal Reserve appears complacent and more focused on the risks to its inflation mandate of the recent tariff hikes

(3) The US Treasury seems to have lost control of the long-end of the bond market, given how rapidly term premia are rising. This will limit the Treasury’s ability to response to any coming crisis

(4) A debt maturity wall is fast-approaching as previously termed-out debts from the COVID-era have to be refinanced from around mid-2025 onwards. This will absorb balance sheet space and deplete Global Liquidity

We have moved ‘Risk Off’ in positioning until we get clear positive signals. Evidence these key fault-lines to monitor:

Crack #1: World Economy Skidding Fast

With latent credit risk embedded in much financial market collateral, a slower World economy poses a huge and negative cyclical risk for Global Liquidity. The following chart is an AI-based daily measure of World GDP growth. It was anyway slowing from mid-December as the US ‘pro-Biden’ stimulus faded, but the latest trade bomb has blasted the World economy into a major skid. The pace of World GDP growth has lost 250bp since end-2024 and recently briefly tested recession.

Crack #2: Fed Reserve Slated to Shrink Its Balance Sheet

The US Fed seem still obsessed with shrinking its balance sheet despite the growing pile of debts that must be refinanced. The swings in the pace of Fed Liquidity this year are largely explained by the debt ceiling and associated gyrations in the TGA (Treasury General Account) plus seasonality. Nonetheless, even if the true underlying liquidity growth trend in near-flat, this is still not supplying anywhere near enough liquidity.

Crack #3: US Treasury Loses Control of Long End of Bond Market

If the US Fed wont ease, the US Treasury in many ways can’t because of the groaning costs of debt finance. The chart below evidences the rising term premia on the 10-year note. Despite on-going fears of recession, US bond term premia are rising, indicating less demand for US safe assets. Higher debt costs will plainly compound so worsening America’s debt outlook.

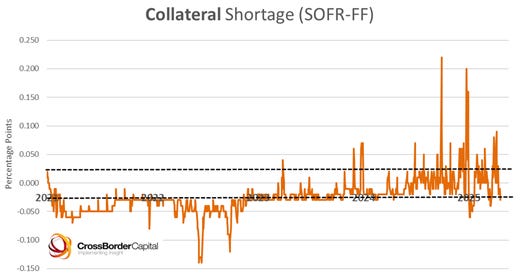

Crack #4: Repo Strains Pick-Up

At the heart of the system, sitting between the pools of liquidity and collateral is the repo market. Some 80% of all credit Worldwide now demands collateral-backing and the repo market is the nexus. Repo market strains are visible when the SOFR less Fed funds spread widens, particularly above the identified tramlines. Some 90% of all repo spread blow-outs have occurred since last July and the bulk of these since the start of 2025. Anyone see a trend?

Policy & Investment Implications

Central Banks: May need to prioritize collateral stability over inflation targets (e.g., quickly restart ‘not-QE, QE’ or expand repo facilities).

Investors:

o Safe Assets: Short-duration Treasuries, gold and the US dollar may outperform amid refinancing chaos

o Credit Risks: Avoid long-duration corporate debt; monitor CRE and shadow banking linkages

Fiscal Authorities: U.S. Treasury may need to issue more short-term bills to ease refinancing pressures, but this could amplify future rollover risks. Long-term, investors should increase their holdings of monetary inflation hedges, namely gold and Bitcoin.

Hi Michael, thanks for the post!

In several of your recent pieces you seemed to be optimistic that liquidity growth in Q1 would support the recovery of bitcoin (and other risk assets?) in Q2 while warning of the risks increasing substantially by Q3-Q4, particularly in terms of money market liquidity running dry.

Given that you now are officially "Risk Off", has anything changed about that thesis? Based on your previous posts, I would have thought that now is a good time to ADD risk to ride the Q1 wave of global liquidity that should hit the markets with a 3-month lag in Q2.

Hey Michael,

Does “risk off” mean you have started selling any of your BTC or other positions? Or rather it means you have just stopped buying? Or something else?

As always, thanks for the quality content!