The Changing Investment Cycle

Re-thinking Asset Allocation

In the past two decades, financial assets have performed strongly, with lately equities again coming into their own. Tangible assets, such as gold and commodities, have delivered more mixed investment returns. We figure much of this relative performance gap can be explained by generally low and falling inflation.

Looking ahead, we fear that although inflation may not rocket higher, we face a future charterised by moderately higher, but more importantly far more volatile inflation rates. If we are correct, asset allocation will need to be carefully rethought.

The Inflation Dimension

Investments can be looked at in two ways: (1) though the performance of underlying securities and (2) from the actions of investors. Ultimately they are the same, but often looking at things from a different dimension adds perspective and insight.

Let’s start with securities: from the end-2013, the World equity P/E multiple has risen from 16.3 to 18 times, with aggregate earnings some 46% higher. Alternatively, consider investors’ behaviour. Their exposure to stocks has barely flickered higher, moving from 0.52 to 0.53 times the pool of liquid assets. Alongside, this Global Liquidity pool has grown by 56%. Viewed through both lens these two ratios (valuation and asset allocation) have changed little, while underlying earnings and liquidity have both grown strongly.

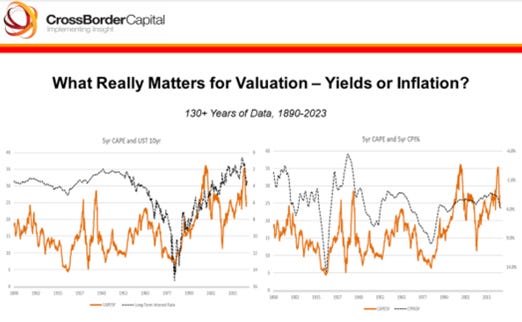

This remarkable stability in asset allocation and valuation ratios is worth pondering. In our view, it is the result of meaningful decline in underlying inflation. Inflation matters hugely for asset allocation and, hence, security valuation because it affects the size of future liabilities. We know that inflation is somehow incorporated into bond yields, but the relationship is far from straightforward and nothing like the textbooks suggest. Ironically, the relationship between stocks and inflation is more straightforward, whereas the relationship between stocks and bonds, much lauded by academics, turns out to be highly complex. Consider, the following charts, using data extracted from the Robert Shiller website:

Keep reading with a 7-day free trial

Subscribe to Capital Wars to keep reading this post and get 7 days of free access to the full post archives.