Global Liquidity Watch: Weekly Update

Falling bond market volatility – an important driver of the collateral multiplier – has provided a fillip to Global Liquidity

Latest weekly data show Global Liquidity inching higher to US$167.1 trillion, just 1% below its earlier peak reading. We have noted in recent weeks the negative effects that volatile bond markets have on collateral values, and hence liquidity conditions. Bond market volatility has subsided – the MOVE index recently hit 130 but has fallen below 100. Added to this the collateral base, the Shadow Monetary Base, also ticked higher this week to US$89.8bn. The two together have helped overall liquidity conditions, but we are mindful that bond markets are likely to remain volatile and need to be monitored carefully.

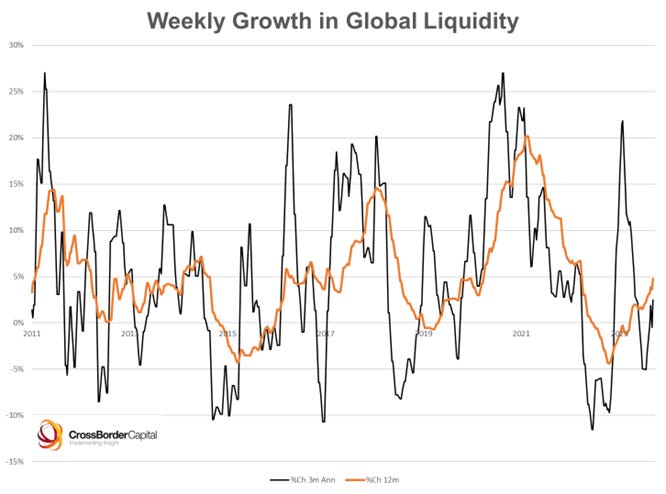

The chart below shows the growth of Global Liquidity year-on-year and on a 3-month annualised basis. It reinforces our view that liquidity conditions bottomed around a year ago. Admittedly, the recovery has been slow and only briefly punctuated by a strong liquidity boost at the time of the SVB crisis.

Source: CrossBorder Capital, US Federal Reserve, People’s Bank of China, ECB, Bank of Japan, Bank of England

Another constraint has been the lacklustre expansion of Central Bank liquidity which directly affects the Shadow Monetary Base. The SMB is expanding (year-on-year) but only gently. (The weak 3-month annualised rate is due to a base effect, viz. the faster growth rate in June and July.) But there are straws in the wind. One is the step-up in liquidity provision by the PBoC; the other is the subtle increase in Fed liquidity. See section on Fed and PBoC.

Keep reading with a 7-day free trial

Subscribe to Capital Wars to keep reading this post and get 7 days of free access to the full post archives.