Global Liquidity

A Different Way to Understand Modern Finance

This short summary is published without a pay-wall to help readers better understand our ‘liquidity-based’ approach. It is theoretical, but practical and has evolved from experience (often hard), starting from the author’s time at Salomon Brothers Inc in the 1980s and 1990s.

The traditional view of financial markets rooted in equilibrium-based models, efficient pricing and fundamental valuation has become increasingly inadequate for explaining modern financial dynamics. Instead, a liquidity-first framework highlights how modern capital markets primarily function as debt-refinancing mechanisms, where crises emerge from collateral shortages rather than asset mis-pricing. This shift demands rethinking our approach to financial stability, central banking and risk management.

Modern economies run on debt, not real investment. And, financial markets are now just liquidity machines that facilitate debt refinancing, where asset prices (P) depend on:

Global Liquidity (L), not fundamentals, and

Risk positioning (P/L), such as duration targeting, passive investment strategies, not valuations

Hence, in our macro-framework:

P= L x P/L

However, finance is fragile. Investors now play a survival game, where Central Bankers and risk managers, not traders, increasingly call the shots. Winning requires tracking liquidity, not earnings. Crises happen when cash flows dry up, not when assets are overpriced. Central banks must keep the system running by backstopping liquidity provision.

Conclusions of the Liquidity-Based View:

1. Financial Markets Are Debt-Refinancing Mechanisms, Not Capital Allocators

Financial markets today are dominated by the need to roll over existing debts, not fund new productive investments

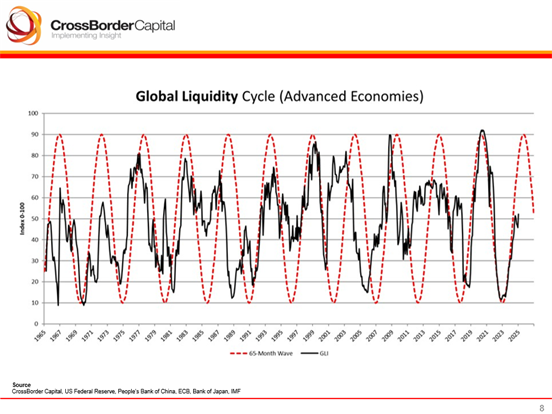

Liquidity (not interest rates) becomes the key driver. This is best thought of as a measure of financial sector balance sheet capacity. It can be quantified by the supply of financial assets relative to their duration, and also by the flow of cash savings and credits through World financial markets

Refinancing walls (e.g., upcoming 2025-28 debt maturities) create cyclical liquidity pressures, explaining the 65-month Global Liquidity Cycle (see chart)

2. Crises Stem from Collateral Shortages, Not Asset Mispricing

Some 80% of lending now involves some form of collateral-backing

Financial instability arises when collateral chains break, not from fundamental overvaluation of assets

Pro-cyclical feedback loops (i.e. unstable collateral multiplier) worsen crises:

Falling collateral values lead to margin calls, fire sales of assets and further liquidity crunches

Rehypothecation of collateral and regulatory constraints

Examples:

o 2008 GFC (MBS collateral collapse)

o 2019 Repo Crisis (sudden money market shortages)

o 2022 UK Gilt Crisis (LDI margin spirals)

3. Central Banks Provide Collateral Backstops, Not Just Inflation Targeters

Modern Central Banking is less about interest rates and more about managing financial plumbing:

o QE provision and ‘Dealer of the Last Resort’ to backstop collateral

o Repo operations to stabilize short-term funding

o FX swaps to cover cross-border dollar shortages

High street inflation is secondary: deflationary collapses (2008, 2020) pose greater risks when liquidity hoarding freezes markets

4. Risk is Systemic and Non-Diversifiable

Traditional finance (CAPM): Risk is diversifiable, assuming idiosyncratic shocks

Liquidity view: Risk is systematic, non-diversifiable and concentrated in collateral chains (e.g., dollar funding, FX swaps, repo markets)

Positioning & duration matter more than valuation:

o Investors target liability-matching durations (e.g., pensions, insurers)

o Regulatory constraints (Basel III, SLR) distort collateral demand

Implications for Policy & Markets:

1. Monetary Policy Must Prioritize Liquidity Over Inflation

QE (quantitative easing) and repo operations are now permanent tools to prevent collateral shortages

US Fed’s ‘higher for longer’ stance on interest rates and headline-QT risk a 2025 liquidity crunch as debt refinancing demands build

2. Fiscal Dominance is Inevitable

Austerity is restricted because it ignores refinancing needs (e.g., Eurozone banking crisis 2010-12)

Interest bill a major fiscal budgetary item: interest costs need to be kept down

Mandatory welfare spending mean structural primary deficits

Sovereign debt markets must be backstopped to prevent systemic collapse (e.g., ECB’s LTRO, BoE’s gilt intervention)

Inevitable resort to ‘easy’ funding via bills and short-dated coupons implies ‘monetization’ of debt

3. Investors Must Track Global Liquidity, Not Just Fundamentals

Safe assets (Treasuries, gold, US dollar) outperform in liquidity crunches

Credit risk is rising, so avoid high yield corporate bonds, watch commercial real estate and closely monitor shadow banking linkages

4. The Dollar’s Role as Global Collateral Creates Structural Vulnerabilities

Some 60% of global trade is dollar-invoiced: US Fed policy drives Global Liquidity

Dollar shortages (e.g., 2008, 2020) can trigger ‘Risk-Off’ regimes

5. Inflation Comes in Different Stripes

High street inflation is different from asset price inflation

Monetary inflation, the deliberate depreciation of paper money by excessive supply, affects both types of inflation

Asset prices are more sensitive to monetary inflation. High street inflation is more sensitive to cost inflation (and cost deflation), e.g. cheap Chinese goods, technology breakthroughs, oil prices and taxes/ tariffs

Conclusion: A Different Financial Paradigm

The liquidity-based framework explains why:

QE did not lead to high street inflation (liquidity trapped in financial assets)

‘Risk-Off’ events trigger dollar squeezes (scramble for collateral)

Central Banks must backstop markets (not just regulated banks)

Monetary inflation (loss of real wealth) is inevitable and more important than ‘financial repression’ (loss of real income)

Traditional economics still has much to say about long-term growth, but the short-term business cycle and financial market stability depend on active liquidity management. The modern financial system is a fragile, collateral-driven mechanism, and one that requires constant intervention to avoid collapse.

Very well done.

bravo, very useful summary. Next step is to incorporate into an AI driven investing platform