Broken China

Part 2: The Collapsing Yen and The Wobbling Yuan

Watershed moments in World financial markets keep on coming. We may be about to see the biggest yet: a major devaluation of the Chinese Yuan? Continuing deflation in domestic goods and asset markets is evidence that China’s real exchange rate is still too high.

There have already been tremors: the persistent weakness of the Yen starkly challenges the wide consensus that has long been calling for a strong rebound in the Japanese currency.

The Yen’s weakness confirms the breakdown of the 2016 Shanghai Accord, which had secretly sought pan-Asian currency stability against the US dollar. We suspect that the Yen has been deliberately weaponized against the Chinese Yuan. Evidence the whopping 2½-fold increase in China’s real exchange rate against the Japanese Yen since 2012. The shadowy Yuan ‘fix’ and the years of struggle to stop capital leaving are China’s key vulnerabilities. Japan may be America’s stalking horse!

Shattering the Shanghai Accord is important because it pushes China into a corner. Consider how past landmark events in international finance subsequently re-shaped the World economy: the August 1971 decision to take the US dollar off gold; the 1974 US ERISA Act, which encouraged international portfolio diversification; the incoming Thatcher Government’s speedy abolition of UK external capital controls in 1979 and the similar liberalization brought in by Japan from 1980, which saw her gross external assets and liabilities quintuple, as a percent of GDP, within the decade.

Accord in Shanghai, Discord in Beijing: The Yuan Exchange Rate

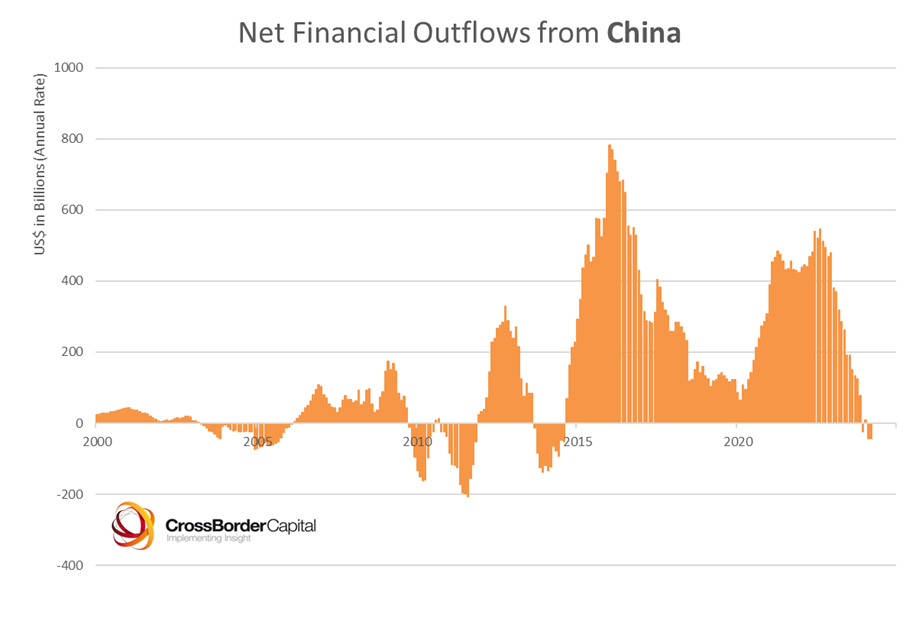

We argued in Part 1 that one lesson from the latest data is that China’s monetary authorities are back in control. Aside from a likely seasonal pick-up later in 2024, Chinese liquidity is largely constrained by the need to manage capital flows and the exchange rate and, at least, to allow the currency to gradually devalue.

Despite capital controls, both foreigners and domestic investors are taking their money out of China. The data shown below highlight an acceleration of outflows from 2015 that coincide with the peak and subsequent slide in the real value of the Yuan.

This on-going international adjustment must occur within the context of what the World monetary system allows. We focused the book Capital Wars (Palgrave, 2020) on three key observations about how this system operates:

• The 1944 Bretton Woods international monetary settlement (aka ‘Bretton Woods I’) still exists with the US dollar as its centerpiece and the IMF, World Bank and US military as its pillars. Notions of a ‘new’ Bretton Woods II and BWIII are simply wrong. And, the claim the Bretton Woods I was simply about re-establishing fixed exchanges rates nothing less than a smoke screen.

• Adjustments to capital flows require changes in ‘real’ exchange rates, but given ‘sticky’ currencies and goods prices, changes are increasingly channeled through asset markets and the financial economy

• China is the major re-exporter of US dollars, but she needs desperately to get off the US dollar hook and establish the Chinese Yuan as an alternative currency of denomination. This is far easier said than done

Indeed, China has long desired a ‘stable Yuan’. This is partly out of fear of making the same exchange rate policy mistakes as Japan in the 1980s, and partly through her desire to foster great regional use of the Yuan as an alternative standard of value to the US dollar. Consider:

…we should promote the Renminbi to be the primary currency of Asia,

just as the US dollar first became the currency of North America

and then the currency of the World …

Every globalization was initiated by a rising empire …As a rising super power, the ‘One Belt, One Road’ strategy is the beginning of China’s own globalization

… it is a counter-measure to the US strategy of shifting focus to the East.

Excerpts from a speech by Major-General Qiao Liang, Chinese PLA, April 2015

The covert 2016 Shanghai Accord to collectively stabilize Asian currency units must be viewed as part of this policy. For almost six years until early-2022 (the break mysteriously aligned with the invasion of Ukraine), Asian currencies demonstrated an unheard of degree of steadiness. The sudden collapse in the Japanese Yen changed that, effectively destroying the notional stability pact. Chinese struggled to keep the Yuan on a level course, but the cost was a sharp tightening of monetary policy. This clashed badly with an economy already reeling under the impact of COVID lock-downs.

Despite these struggles, the market narrative is that the Yuan now needs to revalue higher, based on China’s whopping trade surplus, and a belief that the ‘sneaky’ Chinese are, therefore, trying to get a further competitive edge by devaluating.

But this is wrong. The trade surplus does not reflect greater trade competitiveness. It shows a structural imbalance in Chinese flow of funds, which is the consequence of a low household share of national income. Deflation in domestic goods and asset markets is better evidence that China’s real exchange rate is too high.

The real exchange rate is defined as the nominal exchange rate adjusted multiplicatively by an index of high street prices, wages, and asset prices. Real exchange rates are the main vectors promoting economic adjustment. These adjustments can be slow and drawn out. In practice, wages and high street prices tend to be ‘sticky’ or slower moving than asset prices. Hence, if sufficient pressure builds this can sometimes lead to sudden financial crises.

Such crisis risks are heightened when policy makers are reluctant to let their nominal exchange rates move up or down sufficiently. Typically, policy makers fight against exchange rate strength by easing and, initially at least, they will tighten policy to support a failing currency. Hence, if real exchange rates need to move, but high street prices and wages prove ‘sticky’ and policy makers actively manage exchange rates, then asset markets are forced to take on the bulk of the adjustment burden. This mechanism helps to understand China’s current asset market slump.

In practice, these effects tend to be asymmetric. Exchange rates and asset prices are also prone to overshooting. Policy makers are ultimately more likely to let their currency devalue sharply, than appreciate for trade competitiveness reasons. In other words, asset markets have unlimited upside and enjoy downside support.

Viewed in this way, the many debt-deflations that have hit Asia should be essentially seen as monetary problems. The solution requires a combination of more domestic liquidity creation and a parallel sharp currency devaluation. America escaped the clutches of the Depression by devaluing the US dollar by 40% against gold to US$35/oz through early 1934. Japan’s adjustment has been more drawn out. The Yen hit a post-bubble high of Y84.3/ US$ in May 1995, and even tested Y76.2 in April 2012, before the latest devaluation took it down to Y155/US$ in mid-April, 2024.

China’s on-going deflation and the downward pressure on the nominal Yuan suggest that she is still some way off any equilibrium. The US dollar/ Yuan real exchange rate is reported in the chart below. According to the simple metric, China’s real exchange rate still looks 10-15% too high. Experience shows that the return to an equilibrium real exchange rate can come slowly via domestic deflation, as happened in Japan through most of the period to 2022, or suddenly through a collapsing exchange rate, as in two other recent examples, namely Scandinavia in the early-1990s and emerging Asia in the late-1990s.

This points either to persistent deflation over several years and further weakness in asset markets, or a fall in the Yuan cross to around RMB8/ US$. The more that China intervenes or changes monetary policy to support the Yuan, the more that the required deflationary adjustment is forced through domestic goods and asset prices. But, assuming there are hard social and economic limits to more deflation in China, a nominal Yuan devaluation surely beckons?

We argued in Part 1 than such a devaluation would allow China to substantially expand domestic liquidity. Any spillover of lower Chinese goods prices could also drive down Western inflation rates.

Thanks for heads up. Unfortunately I don't subscribe to their view because gross capital flows dominate and as a result the authors underplay role of banks/ liquidity. Also if you think about it, the big trade surplus economies are the ones where there are fewest class tensions contrary to the theory? In my world ' Capital Wars lead to real Wars'.

Thanks for comments. They need more liquidity to offset deflation. Lower rates would encourage still more debt and might directly threaten the Yuan. I figure they have to continue with fiscal and exports