A Very Different Lens

Macro-Investing Using Liquidity Analysis: A Primer

This report summarizes our different approach to investing and describes how to use Global Liquidity in order to better understand macro-valuation shifts.

An Alternative Model

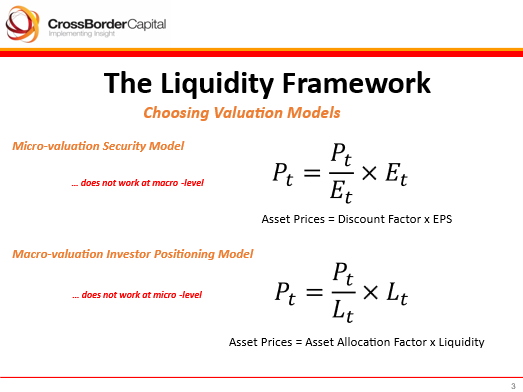

The traditional way to estimate future investment returns is to closely study the attributes of individual fixed income and equity securities. This approach, which focuses, say, on high real yields and low P/E multiples, has a long and successful track record at the security-level. However, its success at the macro-level is highly questionable. In other words, the sum of the individual parts rarely make-up a coherent whole. Something is missing.

To correct this issue, we have developed a different approach. This alternative ‘liquidity-based’ method focuses on the investors, not on the securities. Put another way, we try to understand behavior, not value. And, we study the behavior of both investors and the credit-providers, such as banks and Central Banks, who typically fund them.

Much like traditional analysis, our approach has two moving parts: (1) a behavioral factor that measures asset allocation (P/L) and a (2) liquidity element (L), measuring the inflow and outflow of new money. Contrast this with equity models that start with a value factor (P/E) and multiply this by an earnings forecast (E) to assess prospective returns.

We define ‘liquidity’, using a flow-of-funds methodology, as the flows of savings and credit passing through World financial markets. It is broadly defined to include all credit-providers, not just high street banks, and, because liquidity is ‘fungible’ the appropriate geography is international. Hence, we refer to ‘Global Liquidity’. Another way to think about Global Liquidity is as a measure of the balance sheet capacity of the financial sector. It follows that we often stress the importance of the capacity of capital over the cost of capital, i.e. interest rates. This distinction is particularly important in the current environment where World capital markets act as vast debt refinancing systems, rather than the textbook ideal of new capital raising mechanisms. We have estimated, for example, that 3-in-every-4 trades in World financial markets now involve some form of re-financing transaction.

Keep reading with a 7-day free trial

Subscribe to Capital Wars to keep reading this post and get 7 days of free access to the full post archives.